Summarised below are some of the key operational and financial highlights for the fourth quarter ended 31 March 2024. The commentary on the annual performance is available on the JKH Annual Report 2023/24:

• During the fourth quarter, the Group reported a strong performance across most businesses, with Consumer Foods, Transportation and Leisure, in particular, recording significant growth. The performance seen in most of the businesses is a reflection of the improving macroeconomic conditions in the country and is a continuation of the growth momentum witnessed in the third quarter of 2023/24.

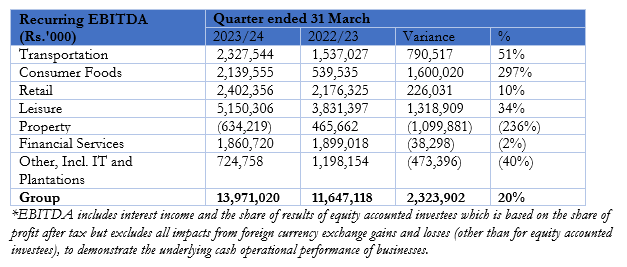

• Recurring Group EBITDA in the fourth quarter of 2023/24 recorded a growth of 20% to Rs.13.97 billion [Q4 2022/23: Rs.11.65 billion]. This growth is despite a higher surplus recognition at UA in the fourth quarter of the previous year due to a timing difference, and the appreciation of the Sri Lankan Rupee by approximately 12%. The average exchange rate was Rs.355 in the fourth quarter of 2022/23 compared to Rs.313 in the fourth quarter 2023/24, which had a negative translation impact on businesses with foreign currency denominated revenue streams. Further, the Group recognised of an asset write-off amounting to Rs.639 million in the Property industry group, as explained below.

• The strong growth in the Transportation industry group was driven by the Bunkering business, Lanka Marine Services, on account of a significant growth in volumes over 50% due to the Red Sea crisis which resulted in an increase in vessel traffic to the coastal waters of Sri Lanka. The Group’s Port and Shipping business, South Asia Gateway Terminals (SAGT), recorded an increase in throughput of 13%. which drove growth in profitability.

• Both the Frozen Confectionery and Beverages businesses recorded strong growth in profitability, driven by improved margins and significant volume increases of 24% and 42%, respectively. It should be noted that volumes in the fourth quarter of the previous year were lower given the reduction in consumer discretionary spend. The volume growth is encouraging, particularly in Beverages, where selling prices of certain SKUs were increased to cover the higher sugar tax and VAT rate increase. Favourable weather conditions, where the country encountered higher than usual temperatures, also supported the growth in volumes.

• Profitability of the Supermarket business was driven by growth in same store sales of 11%, driven by a growth in footfall of 14%. EBITDA recorded growth despite the cost escalations compared to the previous quarter, primarily due to the significant increase in electricity tariffs. The business is expected to see an improvement in energy costs in 2024/25 due to the downward revision of electricity tariffs in March 2024.

• Profitability of the Leisure industry group was driven by a strong recovery in the Sri Lankan Leisure businesses, on the back of a sustained recovery in tourist arrivals to the country, which resulted in higher occupancy and a significant improvement in ARRs across the portfolio. The Maldivian Resorts and Destination Management businesses also saw encouraging growth in EBITDA. The costs pertaining to the ramp up associated with the ‘Cinnamon Life’ hotel at ‘City of Dreams Sri Lanka’ increased on account of the impending opening of the hotel in Q3 2024/25.

• The Property industry group EBITDA includes an asset write-off amounting to Rs.639 million relating to the closure of the ‘K-Zone’ mall in Ja-Ela for the development of the ‘VIMAN’ residential project, resulting in the existing assets becoming redundant. Given the demand for suburban living spaces, the Group is of the view that the project is an optimum monetisation of such land through development and sales. Excluding the asset write-off, the Property industry group EBITDA was Rs.5 million.

• NTB recorded a significant growth in profitability driven by robust loan growth. UA recorded a higher surplus and shareholder profit although this did not reflect in the quarterly performance due to a timing difference of the recognition of the surplus in the previous year which impacted the base.

The full version of the Annual Report is available in the ‘Investor Relations’ section of the Company’s corporate website – https://www.keells.com/resource/reports/annual-reports/JKHPLC_AR_23_24CSE.pdf